eVTOLs (flying cars) set to be one of next year's hot tech trends - here are our Top picks

The rise of urban air mobility inches closer. Now investors, airlines and the DoD are gathering around, but even after 200% rises YTD, eVTOL stocks should have more to give.

Several eVTOL (Electric Vertical Take-off and Landing) companies are scheduled to go commercial in 2024-2025, setting this tech subsector up to be one of next year's big investing trends.

While Archer Aviation (ACHR 0.00%↑) might ship its first aircraft to a paying customer already in Q4 this year, Joby Aviation (JOBY 0.00%↑) looks like the front-runner to get the all-important full FAA certification, which is the final and most important threshold to commercialisation.

Several of the eVTOL startups have also landed big partnership deals, contracts and orders from airlines Delta, United and Virgin, as well as the US Department of Defense (DoD).

With both Archer and Joby upp some +200% YTD, albeit with somewhat differing price action and characteristics, these stocks should have more to give. Let’s take a closer look.

First, are we approaching a Chat GPT moment for aviation?

eVTOLs offer several benefits over existing alternatives:

They're quieter than a helicopter (65-75db compared to 85db for a Bell helicopter at 120m distance, or 50-60db for actual speech).

With multiple rotors to fly, they're also safer than helicopters.

Being electrified, they’re also expected to be cheaper to operate.

But it's not like these machines will outcompete helicopters or airplanes in the near future. However, with that said, there are plenty of niche applications for eVTOLs.

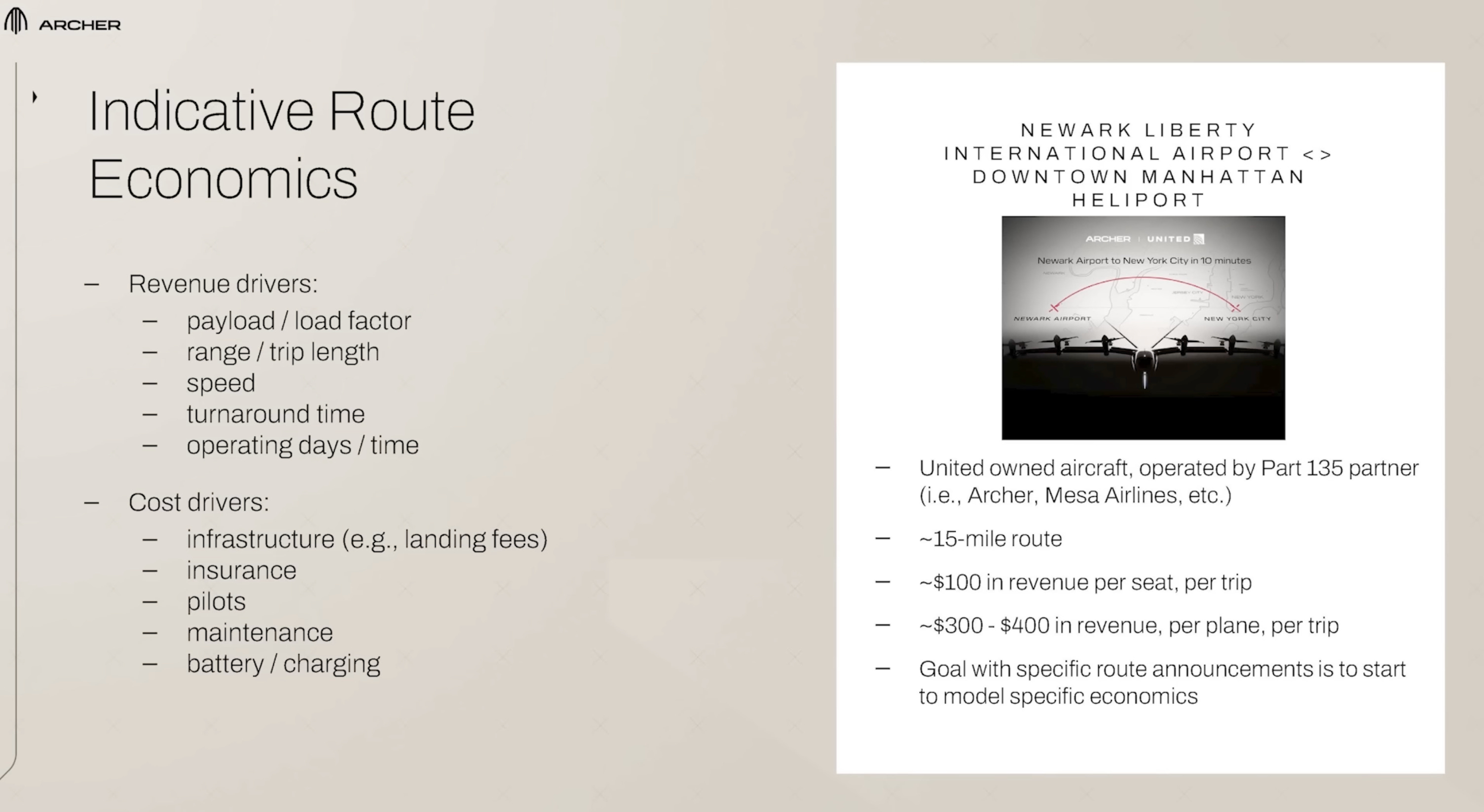

So far, the greatest interest has come from the major airlines, for example Delta, which envisions offering a quick transfer between New York City and JFK and Newark.

Joby is also focussed on offering a UBER 0.00%↑ -like ride-sharing service.

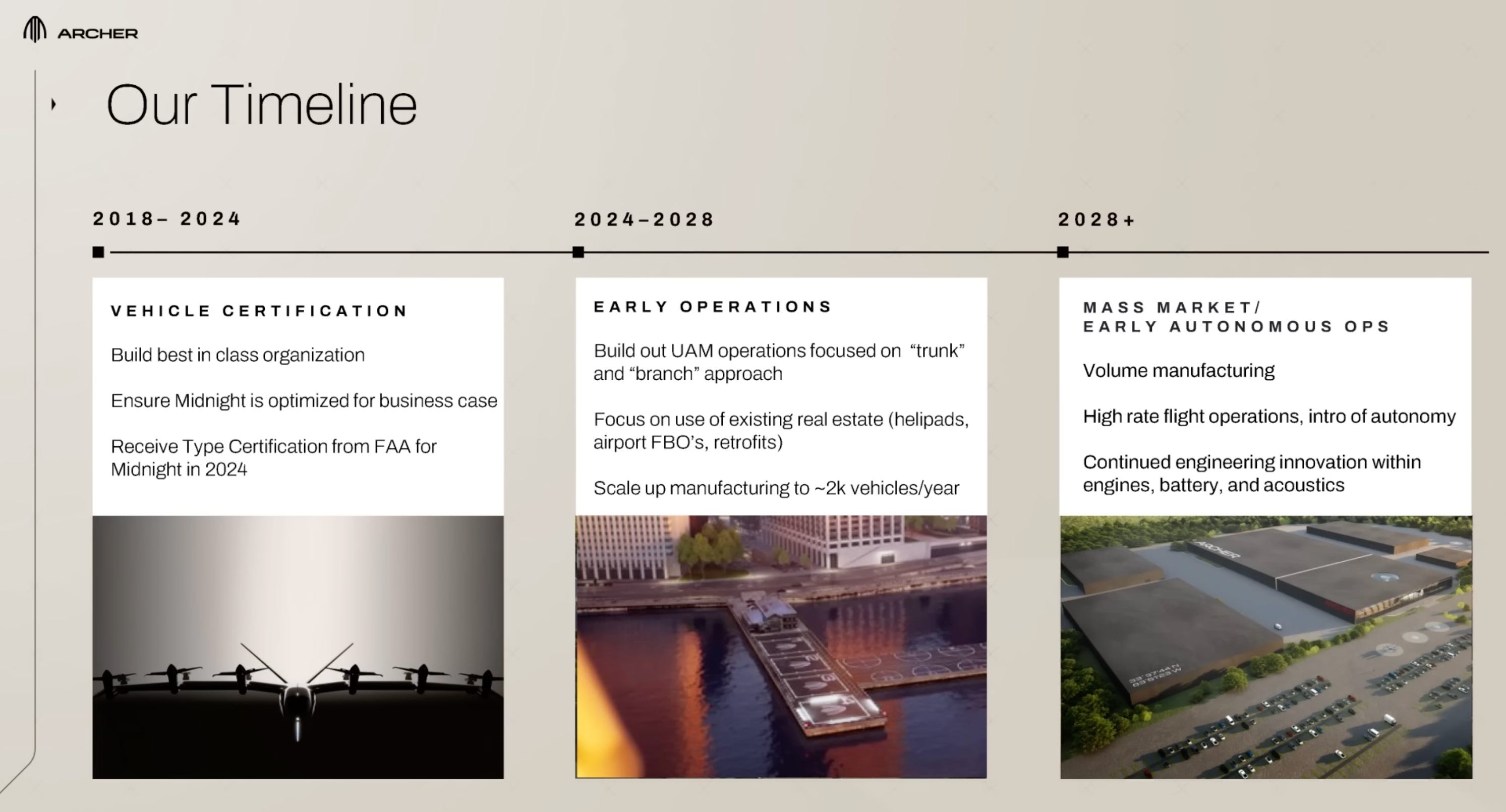

In Archers strategic plan, they expect to scale-up manufacturing to 2,000 vehicles per year in 2024-2028, before reaching mass market manufacturing in 2028.

So while the eVTOLs might be set for a successful roll-out in the coming years, it’s nowhere near ‘flying cars’ or a Chat GPT moment for aviation.

Comparsion Archer, Joby and others

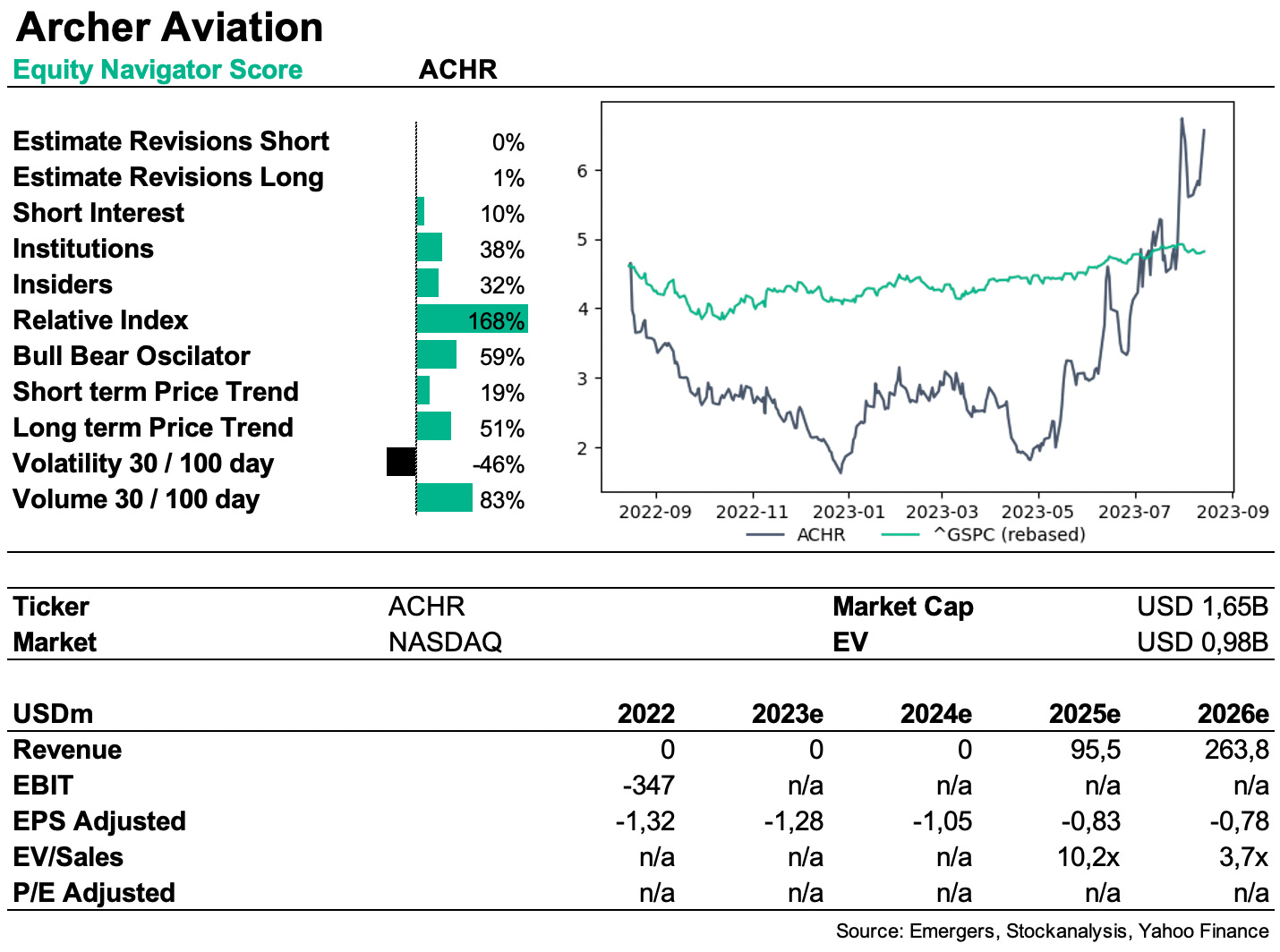

It’s near impossible to look at either Archer or Joby without looking at the other.

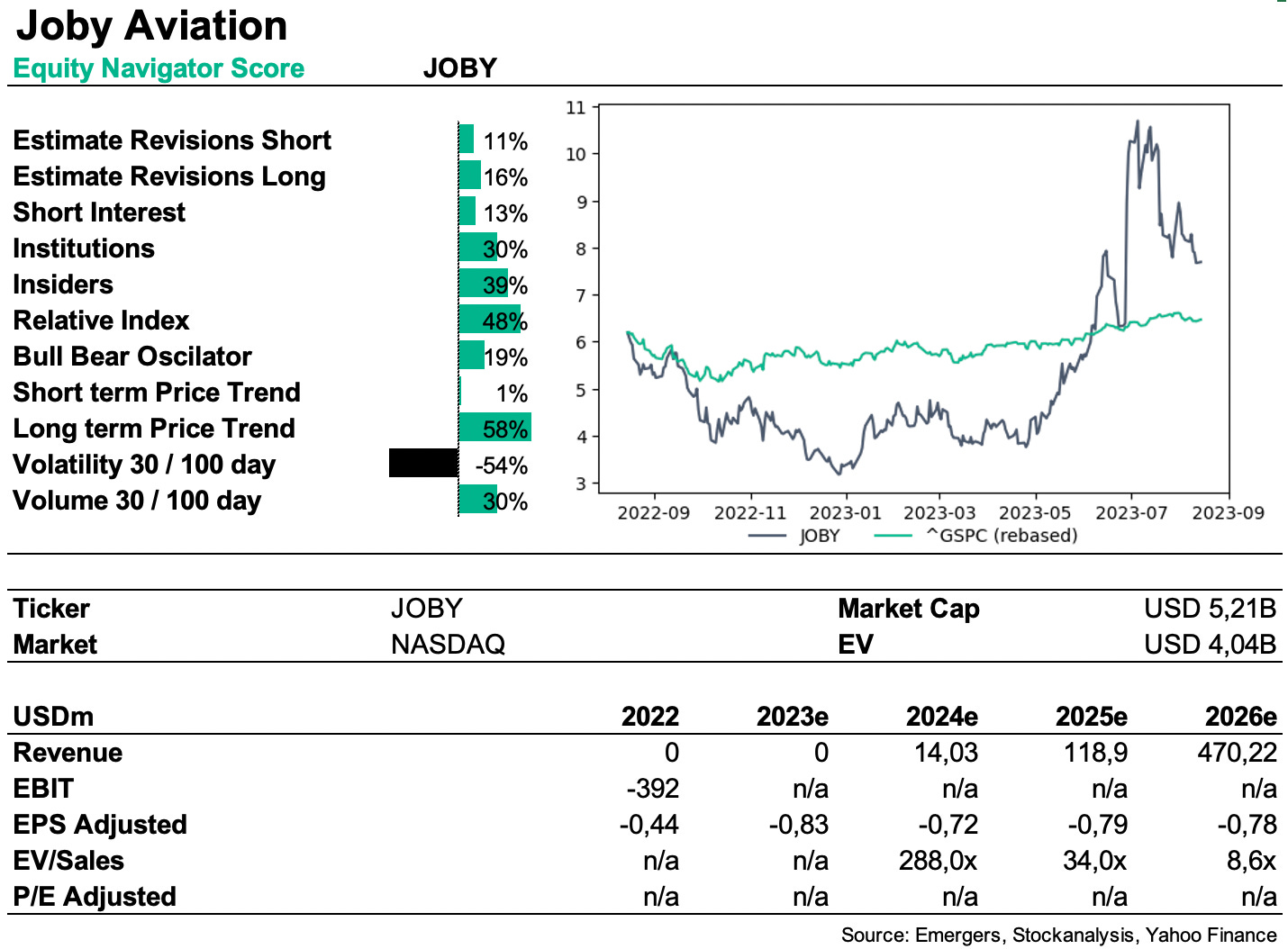

Joby Aviation is no doubt the front-runner in the eVTOL race.

Joby Aviation that is most likely closest to a full FAA certification, with Archer Aviation as close second.

Joby plans an UBER 0.00%↑ -like ride-sharing service.

Plans to go commercial in 2025.

In partnership with Delta Airlines.

Looking at the same data for Archer:

In mid August, Archers vehicle Midnight received FAA Special Airworthiness Certificate, expected to begin flight test and become the first eVTOL aircraft to be delivered to a customer as part of Archer’s contracts with the Department of Defense (DoD).

Plans to go commercial in 2025, but hopes to deliver its first aircraft already in Q4'23.

Has a contract for 300 units with United Airlines.

However, while Joby has flown two relevant sub-scale prototypes, Archer has flown only one. And looking at full-scale representative prototypes, Joby has flown 3 while Archer still has none.

However, these are not the only ones.

Lilium LILM 0.00%↑ is a German #eVTOL startup

Its unusual design uses 36 propellers

Design is similar to jet aircraft will probably make certification easier

Should be the first to win both EU and US flight certification

Plans to go commercial in 2024

Eve Air Mobility EVEX 0.00%↑ is an Embraer spin-off

has a huge 2,800 backlog of orders

leans on Embraer’s expertise in for its technology and the certification process

200 unit contract with United Airlines

Plans to go commercial in 2026

Vertical Aerospace EVTL 0.00%↑ is a British startup

contracts with American Airlines, Virgin Atlantic and Japan Airlines

Plans to go commercial in 2025

Recently crashed a prototype, which caused test flights to halt

However, a lot of it comes down to funding. After a recent cash injection from Boeing, United, Stellantis and ARK Invest, Archer now has USD 675m in cash. But with USD 2+ BN in funding there are good reasons why Joby might beat Archer and the others to commericialisation.

But I doubt that there is much of a first-mover-advantage in the eVTOL market, that is clearly far too big to be filled by one manufacturer alone.

And in light of the USD 5.2 BN market cap for Joby and the USD 1.6 bn market cap for Archer, this suggests that Archer offers the most compelling opportunity.

Shaky business case likely to be revised

As for the actual price of Archer’s Midnight aircraft, they have not pinned down a number yet, but based on the value of the recent defense contract awards to Archer, it breaks down to roughly USD 24m per eVTOL based on the simple math. This however most likely involves some technology exchange and contract work.

In a Forbes interview from March 2023, Archer CEO Adam Goldstein would not reveal the exact unit cost of Midnight, instead putting it at approximately USD 2 m per aircraft. United has ordered 200 of the air taxis with an option for 100 more,

Based on Archer communication we learn that New Yorkers can pay up to USD 1,750 to travel by helicopter from Manhattan to the airport. This Archer and Delta hope to replace with an USD 100 fee per seat, totalling USD 300 - 400 in revenue per plane and trip.

With a generous estimate of 50 trips a day (2 per hour around the clock), this would give a payback period of 1,200 days(!) in the USD 24m per eVTOL example, or 100 days should it be priced at USD 2m per eVTOL.

So even though the price per aircraft will most likely come down substantially from what the DoD is now paying, we should probably expect to pay more than USD 100 per seat to fly from NY to Newark.

Valuation and drivers for a further revaluation

Irrespective of the peer comparsions, what do the valuations look like?

Analyst estimates are roughly similar for Archer and Joby.

For Archer, analysts expects them to reach USD 263m in revenues by 2026e, compared to USD 470m by the same time for Joby. This translates to a 3.7x EV/Sales multiple for Archer in 2026, and 8.6x for Joby.

Both are expected to report losses for the foreseeable future.

Interestingly, both score very good on our proprietary Equity Navigator Scorecard.

Positive to neutral estimate revisions. Short interest at 10% and 13% respectively, despite parabolic rises in the share prices year to date.

Institutional ownership of 38% and 30% respectively suggests that these stocks are still under-discovered by the institutions (compared to tech subsectors Drones and Space, both at around an average 60% institutional ownership each).

Positive momentum and price action, although Joby seems to offer a more compelling entry point then Archer, looking at the chart. Short term (30 days), we’re seeming a pullback in volatility, although volume continues to rise.

All in all, it is clear that

a/ this is an industry that is rapidly approaching commercialization and scale-up

b/ there is still considerable long-term revaluation potential in both these stocks, especially in light of how well-capitalized both are, with strong partners.

c/ It’s hard to find arguments why either of these would be the preferred investment. They both show great promise and potential, and we see a fair chance for continued positive revaluations of both.

However, a final note of caution. As anyone who has ever taken a flight knows, delays are more the rule than the exception in the airline industry.

Disclaimer:

The information on this website is not and should not be construed as investment advice, and does not purport to be and does not express any opinion as to the price at which the securities of any company may trade at any time.

The information and opinions provided herein should not be taken as specific advice on the merits of any investment decision. Investors should make their own decisions regarding the prospects of any company discussed herein based on such investors’ own review of publicly available information and should not rely on the information contained herein.

The information contained on this website has been prepared based on publicly available information and proprietary research. The author does not guarantee the accuracy or completeness of the information provided in this document. All statements and expressions herein are the sole opinion of the author and are subject to change without notice.

Any projections, market outlooks or estimates herein are forward looking statements and are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur. Other events that were not taken into account may occur and may significantly affect the returns or performance of the securities discussed herein. Except where otherwise indicated, the information provided herein is based on matters as they exist as of the date of preparation and not as of any future date, and the author undertakes no obligation to correct, update or revise the information in this document or to otherwise provide any additional materials.

The author, the author’s affiliates, and clients of the author’s affiliates may currently have long or short positions in the securities of certain of the companies mentioned herein, or may have such a position in the future (and therefore may profit from fluctuations in the trading price of the securities). to the extent such persons do have such positions, there is no guarantee that such persons will maintain such positions.

Neither the author nor any of its affiliates accepts any liability whatsoever for any direct or consequential loss howsoever arising, directly or indirectly, from any use of the information contained herein. In addition, nothing presented herein shall constitute an offer to sell or the solicitation of any offer to buy any security.